Navigating Wealth with Precision: The Anand Rathi Approach

Aug 16, 2024

About the company:

Anand Rathi Wealth Limited started as 'Hitkari Finvest Private Limited' on March 22, 1995. It then became 'AR Venture Funds Management Private Limited' on April 6, 2005, and later changed into a Public Limited Company named 'AR Venture Funds Management Limited' on March 8, 2007. Subsequently, it became a Private Limited Company again with the same name on July 7, 2015, then changed back to a Public Limited Company as 'AR Venture Funds Management Limited' on April 3, 2017. It was later named 'Anand Rathi Wealth Services Limited' on July 6, 2017, and finally renamed 'Anand Rathi Wealth Limited' on January 7, 2021.

The company focuses on mutual fund distribution and the sale of financial products within the financial services industry. It caters specifically to High-Net-Worth Individuals (HNI) and Ultra High Net Worth Individuals (Ultra HNI) in India, offering various innovative financial products and investment solutions and also offers non-convertible, market-linked debentures (MLDs).

Business Verticals:

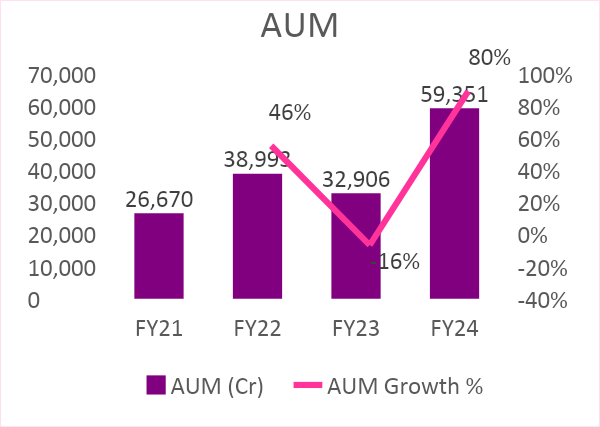

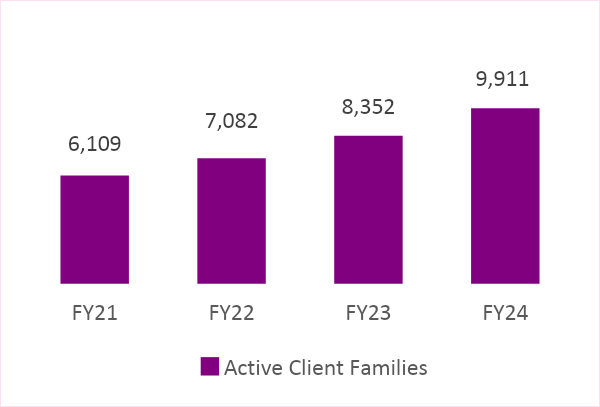

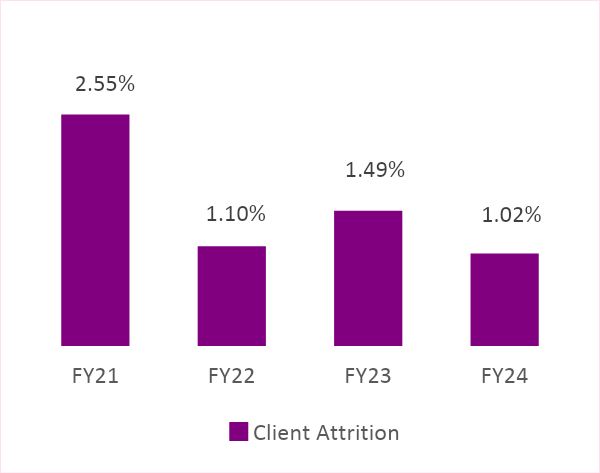

A) Private Wealth: The company caters to the HNI and Ultra HNI in this segment. In FY24, AUM stood at Rs. ~57,800 Cr vs Rs. ~37,900 Cr in FY23. It caters to 10,000+ active client families, serviced by a team of 332 RM's. 60% of its clients have been associated with it for over 3 years, representing 79% of the total AUM. Client attrition in FY24 was 1.0% vs 1.1% in FY23. Having an average of 30 clients per RM.

B) Digital Wealth Segment: The company, through its subsidiary AR Digital Wealth, serves the mass affluent market segment using its 'Phygital' channel. As of FY24, this vertical has an AUM of ~ Rs. 1,500 Cr compared to Rs. 1,000 Cr in FY23. It has 422 client engagement partners and around 4,800 clients.

C) Omni Financial Advisor: Through a subsidiary, FFreedom Intermediary Infrastructure, the company has introduced the OFA vertical, tailored specifically for Mutual Fund Distributors. It caters to the retail segment through a B2B2C model. As of FY24, this segment comprises ~5,900 mutual fund distributors and handles assets of Rs. 1,32,908 Cr of ~20.6 lakh clients.

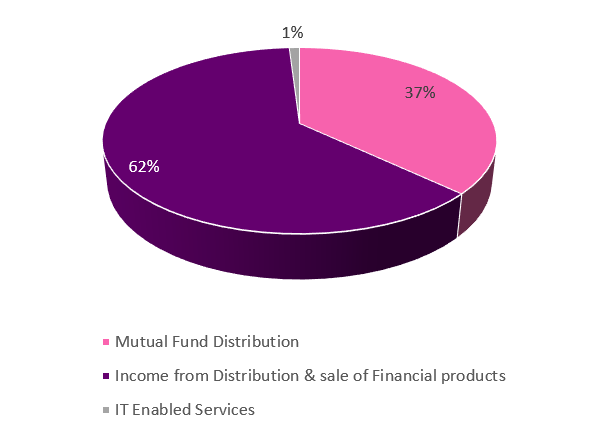

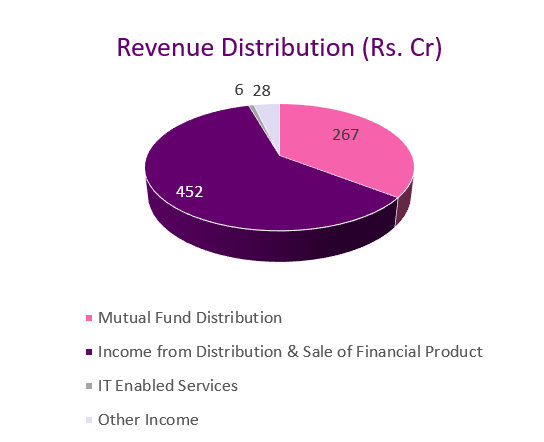

Revenue Mix

Key Points:

The company has been ranked amongst the top 3 non-bank-sponsored mutual fund distributors in India by gross commission earned in FY23.

The company has offices in 17 major Indian cities including Mumbai, Bengaluru, Delhi, Hyderabad, Kolkata, Chennai, Pune, Chandigarh, Jodhpur, Noida, etc, and a representative office in Dubai.

The company has identified an underserved segment within the HNI category- individuals with a net worth between Rs. 5 Cr and Rs. 50 Cr. In FY24, it had 1,559 net new family additions to its client base.

Beyond traditional wealth management, the company offers comprehensive value-added services like estate planning, succession planning, and will creation to its customers.

Management Profiling:

Anand Rathi (Founder & Group Chairman):

Mr. Anand Rathi is the founder and the driving force behind the Anand Rathi Group. He is a gold medalist-chartered accountant and a prominent financial and investment expert in India and the broader Southeast Asian region. Mr. Rathi had a successful career with the Aditya Birla Group, where he was a key member and played a significant role in developing the group's flagship cement business. In 1999, Mr. Rathi was appointed as the president of the BSE (Bombay Stock Exchange). He is a respected member of the ICAI with 53 years of experience across various sectors.

Pradeep Gupta (Co-Founder & Vice Chairman):

Mr. Pradeep Gupta, the co-founder, is the driving force behind the well-established Anand Rathi organization throughout India. He originally started with a family-owned textile business and then ventured into the financial world with Navratan Capital & Securities Pvt. Ltd. After expanding the business, Mr. Gupta teamed up with Mr. Anand Rathi to form the Anand Rathi Group. With over two decades of experience in the financial sector, he has played a key role in the success of the Institutional Broking and Investment Services arms. Additionally, he is an active member of the Rotary Club of Bombay.

Rakesh Rawal (Chief Executive Officer):

Rakesh Rawal joined AnandRathi Wealth Limited as the Chief Executive Officer in 2007. Leading the organization for over 17 years, he is one of the longest-standing CEOs in the wealth management industry. Rakesh has over four decades of experience in the consumer products, engineering, banking, and private wealth industry. He has previously worked with Hindustan Unilever and Deutsche Bank. He earned his bachelor's degree in Mechanical Engineering from the Indian Institute of Technology, Kanpur, and his Master's in Management Studies from Jamnalal Bajaj Institute of Management Studies.

Financials:

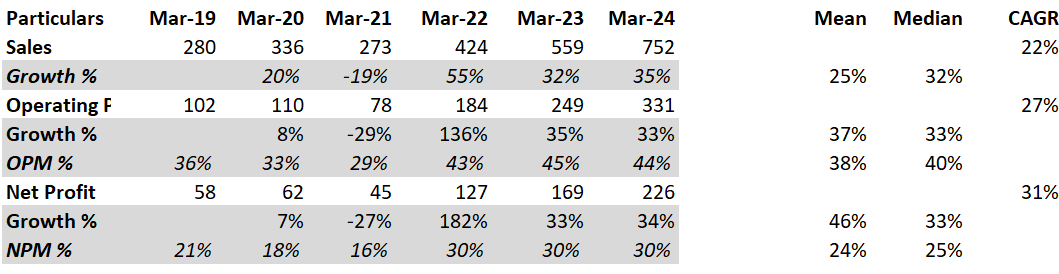

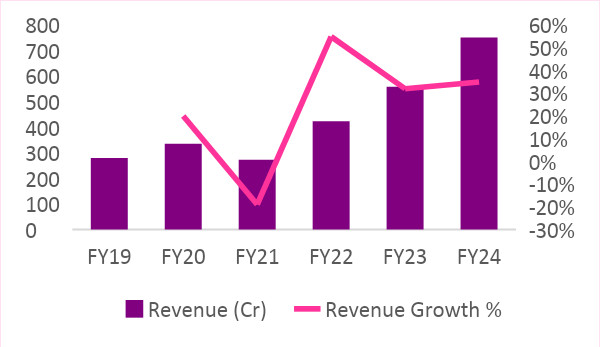

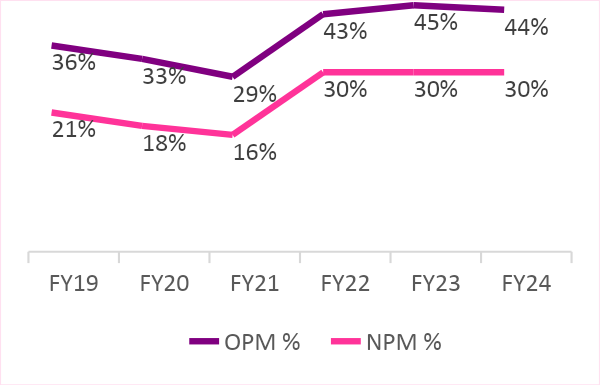

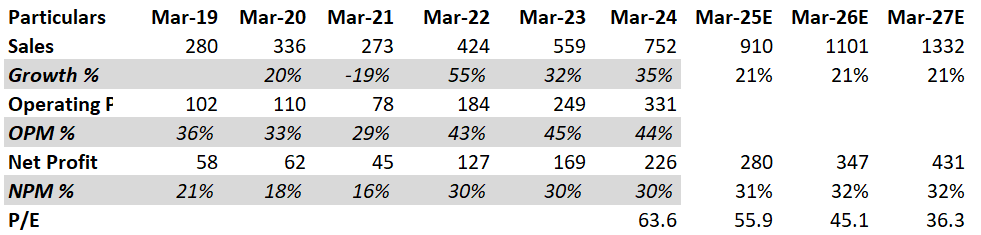

The revenue of the company has grown at a CAGR of 22% in the past 5 years with an average growth rate of 25%, also the company’s revenue registered a growth of 35% to Rs 752 Cr in FY24. The PAT grew by 34% to Rs 226 Cr in FY24 maintaining an NPM of 30%.

The company maintains its growth on four pillars:

Penetration in the existing client families: The company identifies the massive potential for increasing its wallet share within the existing client base of 9,911 families. This indicates a strategic focus on deepening relationships with current clients by offering more comprehensive services and investment products.

Addition of New Clients: In FY24, the company added a net of 1,559 new families to its client base, demonstrating robust growth and a strong endorsement of its wealth management capabilities.

Addition of New Relationship Managers: The company prioritizes expanding its team of Relationship Managers (RMs). In FY24, the company had 332 RMs and 394 Account Managers (AMs), with 122 AMs promoted to RMs over the last five years. The regret RM attrition rate is 0.64% for the year 2023-24, indicating a stable workforce and effective retention strategies.

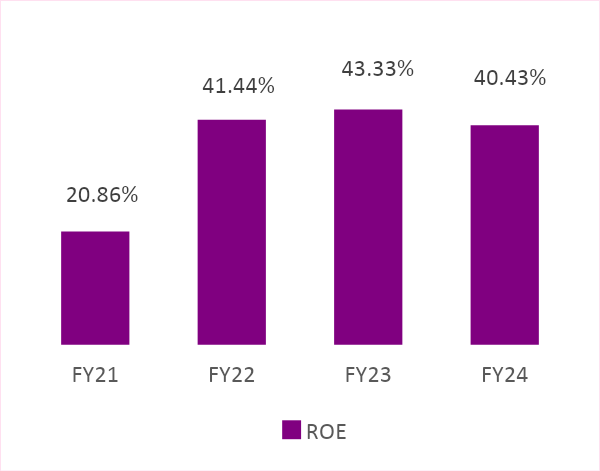

Returns on Investment: The company's private wealth division has consistently achieved positive results in financial planning and investment strategies, leading to a robust return on equity of 40% for FY24.

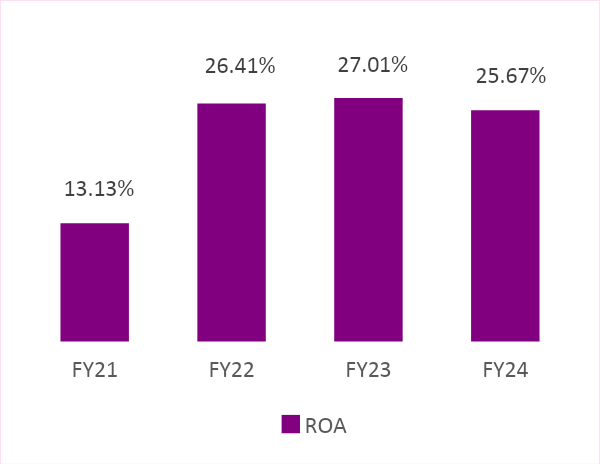

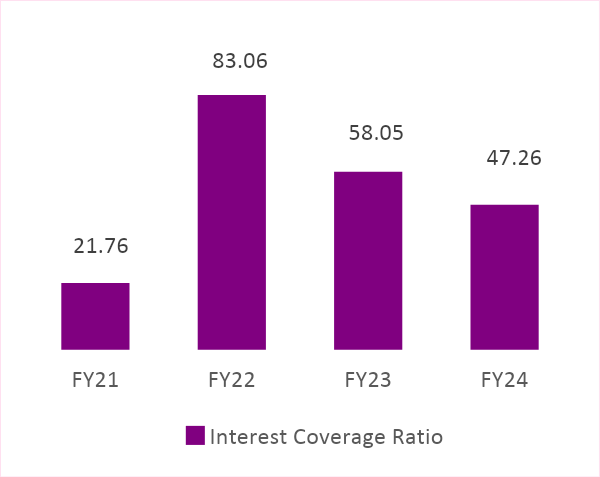

KPIs:

Reasons for the slight fall in ROE:

Increased Equity Base: A significant increase in the company's equity base, through retained earnings or equity infusion, has diluted ROE. While beneficial for long-term growth, a larger equity base can reduce the proportionate returns generated.

Marginal Increase in Net Income: Although ARWL experienced growth in net profit, the increase has not been proportional to the rise in equity. ROE will decrease when the net income growth is slightly slower than the equity growth.

Dip in Asset Turnover: The company's asset turnover ratio has reduced from 0.93x to 0.87x thus, affecting the ROE negatively.

Quarter-on-Quarter:

Looking at the numbers quarterly they have recorded a mean sales growth of 9% over the last 9 quarters which is at par with the average of peers, the company registered an average OPM of 43% over the last 9 quarters which is below the peer average of 49%. Additionally, the company has been able to maintain an average NPM of 31% which is above the peer average of 28%.

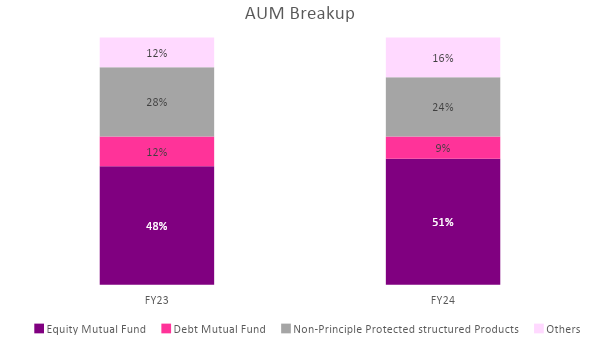

These numbers are driven by strategies such as a strategic focus on reallocating assets between equity mutual funds and structured products. This is due to the lower standard deviation of structured products compared to equity mutual funds.

Despite a strong market, the company plans to strategically reallocate towards structured products, aiming for a proportion of 28-30% by the end of the year.

Some Highlights from con calls of Q4 FY24:

The company aspires to achieve 1 client per Relationship Manager (RM) per month, aiming for a total of 200 new clients per month next year.

Gross sourcing for primary issuance was Rs. 5,182 crores and secondary issuance was Rs. 1,474 crores. The focus remains on maintaining a 40% PBT margin and a 30% PAT margin.

The company focuses on countering cognitive biases like recency bias and influences clients to make well-informed decisions rather than following market trends.

The management plans to add 40-50 relationship managers (RMs) annually, focusing on maintaining quality and cultural fit rather than just increasing numbers.

The digital Wealth segment aims to cater to the mass affluent market, with a 47% year-on-year growth in AUM, highlighting the importance of technology in delivering wealth management solutions.

The management provided a growth guidance of 21% for revenue and 24% for earnings over the next couple of years.

The anticipated asset mix over the next two years includes 30%-35% in structured products, 50%-55% in equity mutual funds, and 8%-10% in debt instruments.

Some Highlights from con calls of Q1 FY25:

The Indian economy is projected to grow at 7.2%, positioning it as one of the fastest-growing markets globally. This growth is expected to increase the number of high-net-worth individuals, presenting significant opportunities for the wealth management sector.

The collateral service will continue without charges as it does not impact revenues directly but significantly strengthens the client's affection towards the company.

When asked about the increment in RM productivity the management said RM productivity can increase as RMs give away smaller clients to their apprentices, who then become RMs themselves. This cycle allows the RM to take on more significant clients, thus increasing overall productivity without saturation.

The trend of money flowing from old to new clients varies with market conditions. During favorable markets, new client acquisitions increase, while in tepid markets, the focus is more on existing clients. The company adjusts its strategies based on these cycles.

Ring-fencing is crucial for HNIs to protect their wealth from external liabilities. The company has been providing this service for free for many years, as part of their client-centric approach. Additionally, Anand Rathi Wealth has facilitated about 6,000 wills, ensuring comprehensive estate planning without charging clients for these essential services.

The management expressed confidence in achieving a long-term growth rate of 20% to 25%, driven by the company’s robust performance and market conditions.

Projections:

As per the latest con call held by the company, the management has given a growth guidance of 21% revenue over 2-3 years and maintaining an average net profit growth of 24% over a similar period thus the above projections of topline and bottom line have been made as per the management guidance. This growth maintains the same share price next year the share will be available at a P/E of 55.9x next which would cool down to 45.1x in FY26.

Valuations:

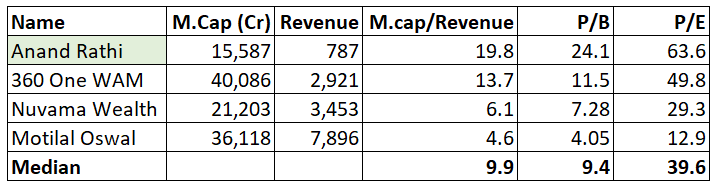

The company is fundamentally performing well and experiencing healthy growth at a rate of over 20%. They are exploring new business areas and continually adjusting their asset mix strategy based on market conditions and customer needs. However, the company appears to be relatively expensive compared to its peers in terms of valuation.

Technical:

Overvaluation of the company seems to be playing out on the chart as the stock price has met resistance at the price level of Rs 4,280 on three occasions which seems to be the rejection zone on the current market condition from there it came down to Rs 3,778 showing some signs of weakness. The RSI index shows a very low strength of 41.63 on the daily chart which further indicates a loss of momentum in the stock. The price can go to the low of Rs 3,416 which appears to be a previous support zone.

Stay Connected, Stay Informed –

Don’t miss out on exclusive updates, market trends, and real-time investment opportunities. Be the first to know about the latest unlisted stocks, IPO announcements, and curated Fact Sheets, delivered straight to your WhatsApp.