Navi Technologies Financial Payment Fraud: Insights Into the ₹14.26 Crore Scam and Its Impact

Feb 18, 2025

A Case Based on Payment Gateway Vulnerabilities & the growing threat to fintech

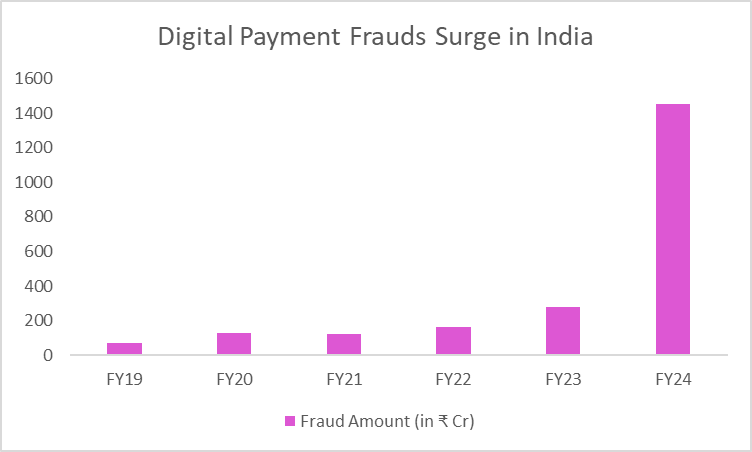

Over the last decade, the rise and significant surge of digital payment platforms and fintech solutions has revolutionized how we manage money and India’s rapid shift to digital payments has been transformative. Due to this transformation we experienced an instant switch to digital online payments. It is good from a technology aspect. However, this transformation has come up with an alarming growth in financial fraud. According to a report by the Reserve Bank of India, digital payment frauds skyrocketed more than fivefold in FY24 alone, reaching an incredible ₹14.57 billion (₹1,457 crore), in comparison to the previous period.

This surge comes as India has ended up a digital payments leader for the reason that the launch of the Unified Payments Interface (UPI) in 2016, permitting customers and users to transfer money immediately through mobile phones. Over the past two years, the value of UPI transactions has seen an astounding 137% growth, crossing ₹200 trillion in 2023. According to the RBI report, the lower priced or we can say affordable to some extent internet and better access to financial services have presented a massive position in this increase, however they have additionally led to more fraud cases.

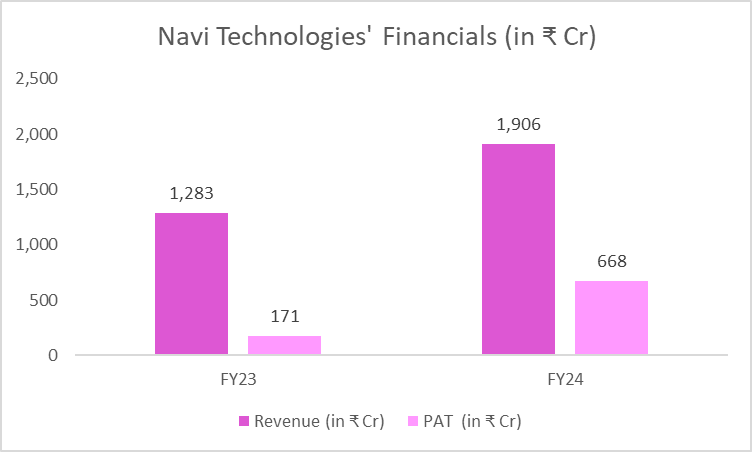

Frauds within the fintech industry are not simply financial mishaps; they may be large breaches of trust and integrity. Recently, Navi Technologies, co-founded by Sachin Bansal of Flipkart fame, have become the victim of an intricate elaborate scam that cost the company ₹14.26 crore. This case exposes the vulnerabilities inherent in fintech operations, specifically at times of handling and dealing with third-party payment gateways. As startups like Navi Technologies attempt to revolutionize financial offerings, this incident underscores the importance of strong and robust security measures.

About Navi Technologies

Founded by Sachin Bansal in 2018, Navi Technologies makes a speciality of simplifying financial services for the Indian market. Its key offerings include:

Personal and Home Loansthat operated through its NBFC subsidiary, Navi Finserv, providing unsecured loans with major competitive interest rates.

Insurance Products that include health and life insurance to cater to India’s growing insured population.

Investment Platforms that offer significant access to mutual funds and other different investment products through its mobile app.

About the Recent Case: What Happened at Navi Technologies?

In a recent sophisticated scam, fraudsters exploited a loophole in Navi Technologies' payment system. Using a third-party payment gateway, scammers manipulated transaction amounts, marking payments as a success for an insignificant and mere ₹1 while the company was actually charged the full transaction amount. The malicious program or bug allowed them to siphon off funds undetected till the total losses reached ₹14.26 crore. The lack of robust monitoring mechanisms allowed the fraud to go ignored until massive losses amassed.

This incident comes at a critical time for Navi Technologies:

RBI Scrutiny: In October 2024, the Reserve Bank of India (RBI) directed Navi Finserv to pause mortgage and loan disbursements over concerns regarding high interest rates. Navi finally diminished its interest rates from 35% to 26%, regaining RBI approval in December.

Complaint Filed in Bengaluru

A formal complaint lodged with the Whitefield Cybercrime Police in Bengaluru to investigate the breach. Cybercrime specialists have noted this as a wake-up call for fintech corporations, emphasizing the importance of often trying out their systems for potential vulnerabilities. This emphasizes the careful and regular testing for the system.

Industry Implications: Why This Matters to Fintech

This case is not isolated. Payment fraud is one of the biggest threats to fintech startups globally. As fintech adoption accelerates, so do the risks:

Scale of Losses: Fraudulent activities can quickly scale up in an industry that procedures millions of microtransactions every day.

Customer Distrust: Once trust is compromised, regaining it could take years and large marketing attempts as well as efforts.

Regulatory Backlash: High-profile frauds often invite stricter guidelines, increasing compliance burdens for startups.

Investigations Underway

Authorities have initiated a research to track the culprits and proper investigation was conducted. This overall presentation of the case underscores the growing sophistication of cyber fraud in India’s rapidly developing digital payment system and reveals the importance of tightening the system's check for safer payment transactions.

To address this growing risk, the RBI has intensified and bolstered its efforts to promote financial awareness by providing financial literacy to deal with frauds. High-profile campaigns, including the ones presenting Bollywood icon Amitabh Bachchan, aim to train users about the risks of online financial transactions and the significance of stable and secure payment practices.

Steps Taken Post-Fraud

Navi Technologies has reportedly initiated an intensive research and taken corrective measures to save you future incidents:

System Audits: Comprehensive audits of payment structures to pick out and rectify vulnerabilities.

Partnership Review: Reevaluating agreements with third-party service vendors to ensure compliance with the best protection standards.

Fraud Insurance: Exploring insurance options to mitigate the financial effect of comparable and similar incidents within the future.

Addressing Cyber Threats in Fintech: Need of the Hour

This case underscores the urgent requirement for sturdy cyber defences in fintech. Key instructions include:

Strengthening Payment Gateways: Ensuring payment gateways can not be manipulated by users post the transaction initiation.

Real-Time Fraud Detection: Leveraging AI and machine learning mastering to stumble on and block suspicious activities right away.

Third-Party Audits: Conduct regular security audits of third-party integrations like TPAPs to ensure safety that is most important for today’s time.

Conclusion

The ₹14.26 crore cyber fraud at Navi Technologies serves as a cautionary story for India’s continuously evolving fintech sector. While the corporation remains a key participant, the incident emphasizes the significance of cybersecurity in terms of building trust and resilience. As digital finance continues to grow, strong systems, proactive measures, and vigilant oversight might be essential for shielding both companies and customers.

Stay Connected, Stay Informed –

Don’t miss out on exclusive updates, market trends, and real-time investment opportunities. Be the first to know about the latest unlisted stocks, IPO announcements, and curated Fact Sheets, delivered straight to your WhatsApp.