Indian startup funding hits a record low in 2023: A year end review

Jan 1, 2024

A year end review

As we bid adieu to 2023, it's crucial to reflect on the journey of India's startup ecosystem throughout the year. In a landscape known for its highs and lows, the year brought about a significant twist – a record low in startup funding.

The year 2023 witnessed highs and lows, as it faced multiple headwinds that affected the funding activity and the growth prospects. While some startups achieved milestones, such as becoming unicorns, going public, or expanding globally, others faced hardships, such as layoffs, shutdowns, or pivots. The most notable trend of the year, however, was the funding winter.

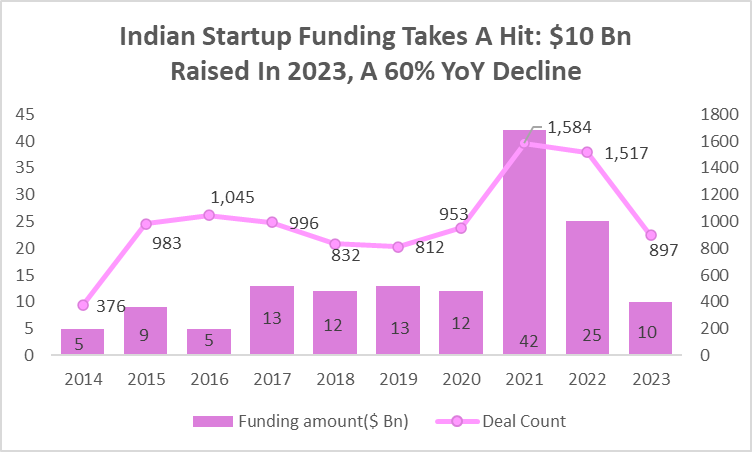

According to a report by Inc42 Media, the total funding raised by tech startups in 2023 was $10 billion, a 60% drop from 2022 and a 76% fall from the peak in 2021. This was the lowest level of funding in seven years, since 2016. The number of deals also fell by 40%, from 1,185 in 2022 to 713 in 2023.

The funding crunch had a severe impact on the Indian startup landscape, as many startups had to resort to cost-cutting measures, such as layoffs, salary cuts, and pivots, to survive. According to a report by Tracxn, over 16,000 employees lost their jobs in the Indian startup sector in 2023, a 60% increase from 2022.

Startups have been narrowing their employee count as India saw another cycle of drying up funding since last year to bring the focus back on profitability and reducing cash burn. Consequently, India dropped from 4th place in 2022 and 2021 to 5th place among the highest-funded geographies globally in 2023.

Stage-wise Analysis

The funding activity in 2023 also varied across different stages, with some stages witnessing a surge in funding, while some others experiencing a decline.

The Startup funding stages can be classified into categories: seed stage, growth stage, and late stage. The seed stage refers to the initial funding raised by startups, usually between ₹1 cr to ₹5 cr. The growth stage refers to the funding raised by startups that have achieved product-market fit and are scaling up, usually between ₹5 cr to ₹250 cr. The late stage refers to the funding raised by startups that are close to profitability or exit, usually more than ₹250 cr to upto ₹4000 cr.

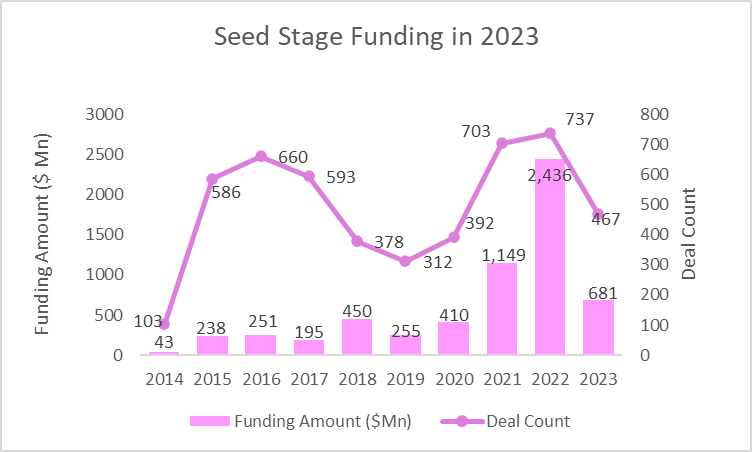

Seed stage:

According to the report Inc42, the seed stage funding raised from 2014 to 2023 is ~$6Bn and reports 72% YOY decline in 2023. The number of seed stage deals also declined by 55%, from 737 in 2022 to 467 in 2023. The seed stage funding was the worst hit by the funding crunch, as investors became more risk-averse and focused on their existing portfolio companies. The average ticket size of seed stage funding also decreased by 31%.

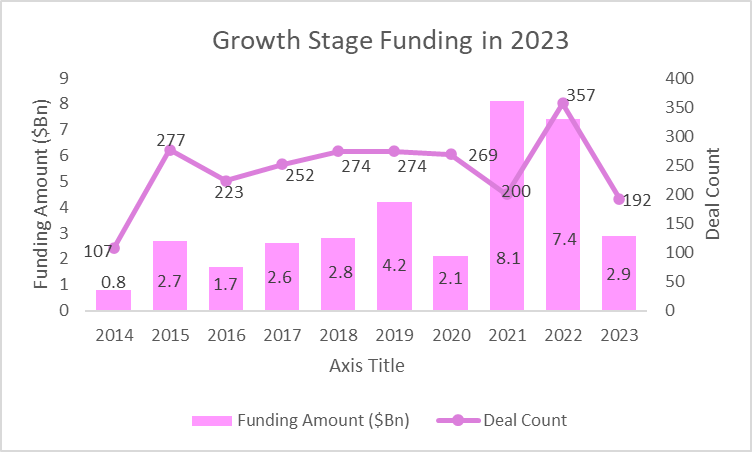

Growth stage:

The growth stage funding in 2023 was $7.8 Bn, a 72% drop from the $28.8 Bn in 2022. The number of growth stage deals also declined by 57%, from 357 in 2022 to 192 in 2023. The growth stage funding was the most affected by the funding crunch, as investors became more skeptical and demanding of the startups’ unit economics, profitability, and valuation. The average ticket size of growth stage funding also decreased by 45%, from $169.4 Mn in 2022 to $94 Mn in 2023. Indian startups witness a 60% correction in growth stage funding.

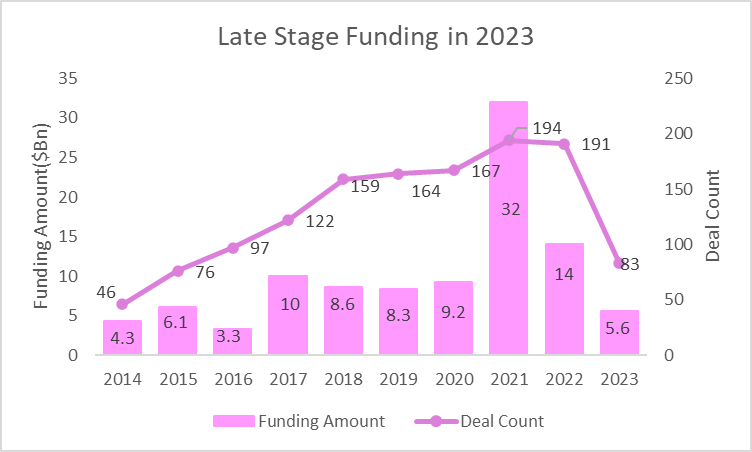

Late stage:

The late stage funding in 2023 was $3.5 Bn, a 79% drop from the $16.7 Bn in 2022. The number of late stage deals also declined by 64%, from 28 in 2022 to 10 in 2023. The late stage funding also suffered from the funding crunch, as investors became more wary of the high valuations and exit prospects of the startups. The average ticket size of late stage funding also decreased by 42%, from $596.4 Mn in 2022 to $350 Mn in 2023.

Investment in late and growth-stage startups decelerated due to a discerning strategy adopted by private market investors. The decline in funding for the current year is mainly linked to a significant drop in late-stage deals (Series D and beyond), plummeting from $11.70 billion in 2022 to $3.5 billion in 2023.

Sector-wise analysis

The funding activity in 2023 varied across different sectors, with some sectors witnessing a surge in funding, while some others experiencing a decline. According to Inc42 Media, the top five sectors that attracted the most funding in 2023 were fintech, edtech, ecommerce, enterprise tech, and healthtech.These sectors accounted for 77% of the total funding amount in 2023.

Fintech: The fintech sector emerged as the most funded sector in 2023, with $3.8 Bn raised across 180 deals This was a 20% increase from the $3.2 Bn raised in 2022. The fintech sector benefited from the increased adoption of digital payments, lending, insurance, and wealth management solutions, especially during the Covid-19 lockdowns. Some of the notable funding rounds in the fintech sector include Paytm’s $1 Bn round in November 2023, Razorpay’s $100 Mn round in June 2023, and Pine Labs’ $300 Mn round in May 2023.

Edtech: The edtech sector was the second most funded sector in 2023, with $2.3 Bn raised across 80 deals. This was a whopping 182% increase from the $820 Mn raised in 2022. The edtech sector witnessed a huge demand for online learning solutions, due to the pandemic. Some of the notable funding rounds in the edtech sector include Byju’s $400 Mn round in January 2023, Unacademy’s $150 Mn round in September 2023, and Vedantu’s $100 Mn round in July 2023.

Ecommerce: The ecommerce sector was the third most funded sector in 2023, with $1.9 Bn raised across 120 deals. This was a 67% decline from the $5.8 Bn raised in 2022. The ecommerce sector faced several challenges, such as supply chain disruptions, regulatory hurdles, and competition from offline retailers, which affected its funding activity. Some of the notable funding rounds in the ecommerce sector include Udaan’s $585 Mn round in February 2023, Nykaa’s $100 Mn round in March 2023, and Grofers’ $220 Mn round in May 2023.

Healthtech: The healthtech sector was the fifth most funded sector in 2023, with $1.4 Bn raised across 110 deals. This was a 40% decline from the $2.3 Bn raised in 2022. The healthtech sector faced some challenges, such as regulatory uncertainties, data privacy issues, and low consumer trust, which affected its funding activity. However, the sector also witnessed some opportunities, such as telemedicine, online pharmacy, and preventive healthcare, which attracted some funding. Some of the notable funding rounds in the healthtech sector include Cure.fit’s $110 Mn round in April 2023, Pharmeasy’s $220 Mn round in November 2023, and Practo’s $100 Mn round in August 2023.

How Startups & Investors Can Thrive In The Funding Winter

The funding winter is a term used to describe a period of reduced venture capital activity and investment in startups, usually caused by external factors such as economic slowdown, geopolitical tension, regulatory uncertainty, or market saturation. The Indian startup ecosystem experienced a severe funding winter in 2023, when the total funding raised by tech startups dropped to a seven-year low of $10 billion, down 60% from 2022 and 76% from the peak in 2021.

However, the funding winter is not necessarily a doom-and-gloom scenario for startups and investors. In fact, it can be an opportunity to adapt, innovate, and emerge stronger in the long run. According to a report by Razorpay, the funding winter can be a chance for startups to focus on extending their runway, reducing their burn rate, generating revenue, and achieving profitability. Similarly, the funding winter can be a chance for investors to find solid investment opportunities, diversify their portfolio, and support the startups that have proven their product-market fit, scalability, and resilience.

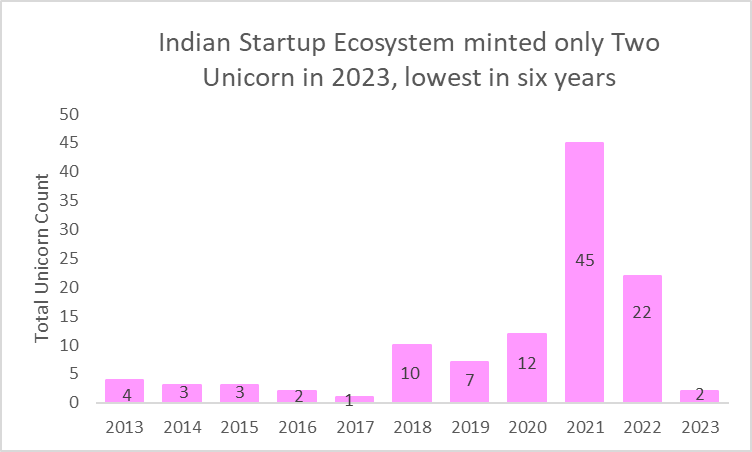

However, not all was gloomy in the Indian startup scene, as some startups managed to raise funds, grow, and even achieve the coveted unicorn status. A unicorn is a startup that is valued at over $1 Bn. According to Inc42 Media, only two Indian startups became unicorns in 2023, namely Zepto became India’s first 2022 unicorn with $200 million fresh funding in August 2023 and Incred Finance, became the second one with Rs 500 crore funding in December 2023.

The Outlook for 2024

The outlook for 2024 is mixed, as some experts predict a potential rebound in the funding activity, while some others remain cautious. The Indian startup ecosystem is undergoing a phase of correction and consolidation, as the funding winter forces the startups to focus on their unit economics, customer retention, and revenue generation. The startups that can adapt to the changing market conditions, innovate their products and services, and create value for their stakeholders, will be the ones that will survive and thrive in the long run. The startups that can also leverage the emerging opportunities in sectors such as edtech, fintech, healthtech, and agritech, will be the ones that will lead the next wave of growth and innovation in the Indian startup space.

Stay Connected, Stay Informed –

Don’t miss out on exclusive updates, market trends, and real-time investment opportunities. Be the first to know about the latest unlisted stocks, IPO announcements, and curated Fact Sheets, delivered straight to your WhatsApp.